2026 // BINARY OPTIONS & EXPECTED VALUE

BTC 5-Min Expected Value

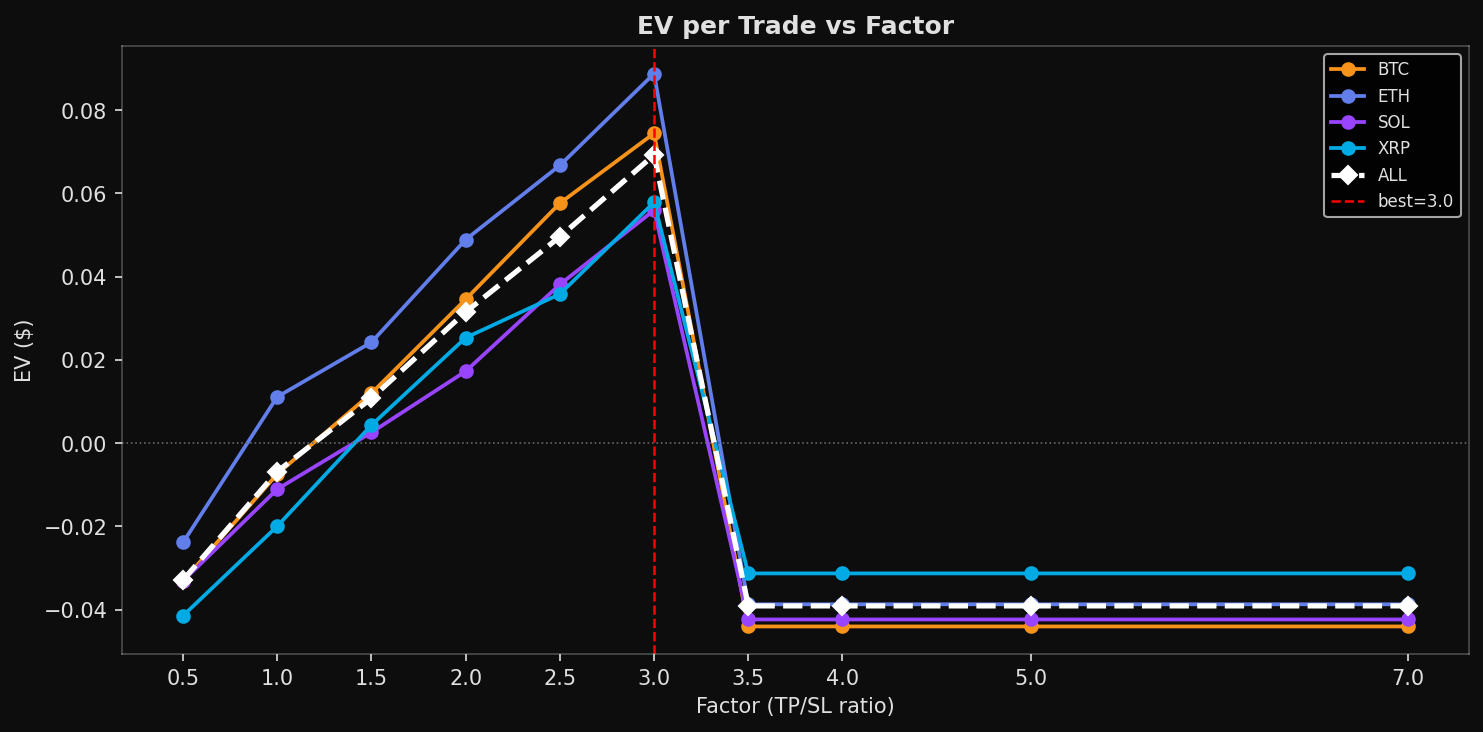

Backtesting a positive-EV strategy on 5-minute binary option contracts across BTC, ETH, SOL, and XRP using real Chainlink oracle data.

I research quantitative finance and computational modeling, focusing on stochastic volatility models and Monte Carlo simulations, and I develop and test models using Python and C++.

From mathematical finance to production.

Translating stochastic calculus into production-grade C++, robust, documented, and benchmarked.

Python-driven testing of pricing models against market data with statistical rigor.

Designing, coding, and validating strategies grounded in stochastic methods.

Backtesting a positive-EV strategy on 5-minute binary option contracts across BTC, ETH, SOL, and XRP using real Chainlink oracle data.

Real-time limit order book analysis and paper-trading system streaming live Deribit data through four competing microstructure strategies.