BTC 5-MIN EXPECTED VALUE

Backtesting a positive-EV strategy on 5-minute binary option contracts across BTC, ETH, SOL, and XRP using real on-chain price data from Chainlink oracles. The strategy exploits the symmetric pricing of binary contracts with an asymmetric risk/reward exit rule.

Go to Repo Read Blog

THE IDEA

Binary options resolve to $1 (win) or $0 (lose). At the start of every 5-minute contract, both UP and DOWN are priced near $0.50 — a fair coin flip. The strategy exploits this symmetry by applying an asymmetric risk/reward exit rule: a tight stop-loss and a wide take-profit, so that each win pays multiples of each loss.

| Parameter | Value |

|---|---|

| Entry | $0.50 |

| Stop Loss | $0.35 (risk = $0.15) |

| Take Profit | Variable (factor sweep) |

| Side | Random (UP or DOWN, seeded per contract) |

The strategy doesn't need to win often — it just needs the asymmetry to compensate for the lower hit rate. For a 3:1 factor (TP = $0.95), the theoretical EV per trade is +$0.15.

DATA & METHODOLOGY

Each contract is stored as a JSONL file with three record types: a header containing contract metadata (asset, condition ID, start/expiry times, strike price), tick-level state snapshots (bid/ask for UP and DOWN, Chainlink price, seconds remaining), and a footer with the resolution outcome.

The dataset comprises ~572 contracts across 4 crypto assets, collected in March 2026. A cleaning step drops all ticks where the Chainlink price is null, removing stale data from contract-open lag.

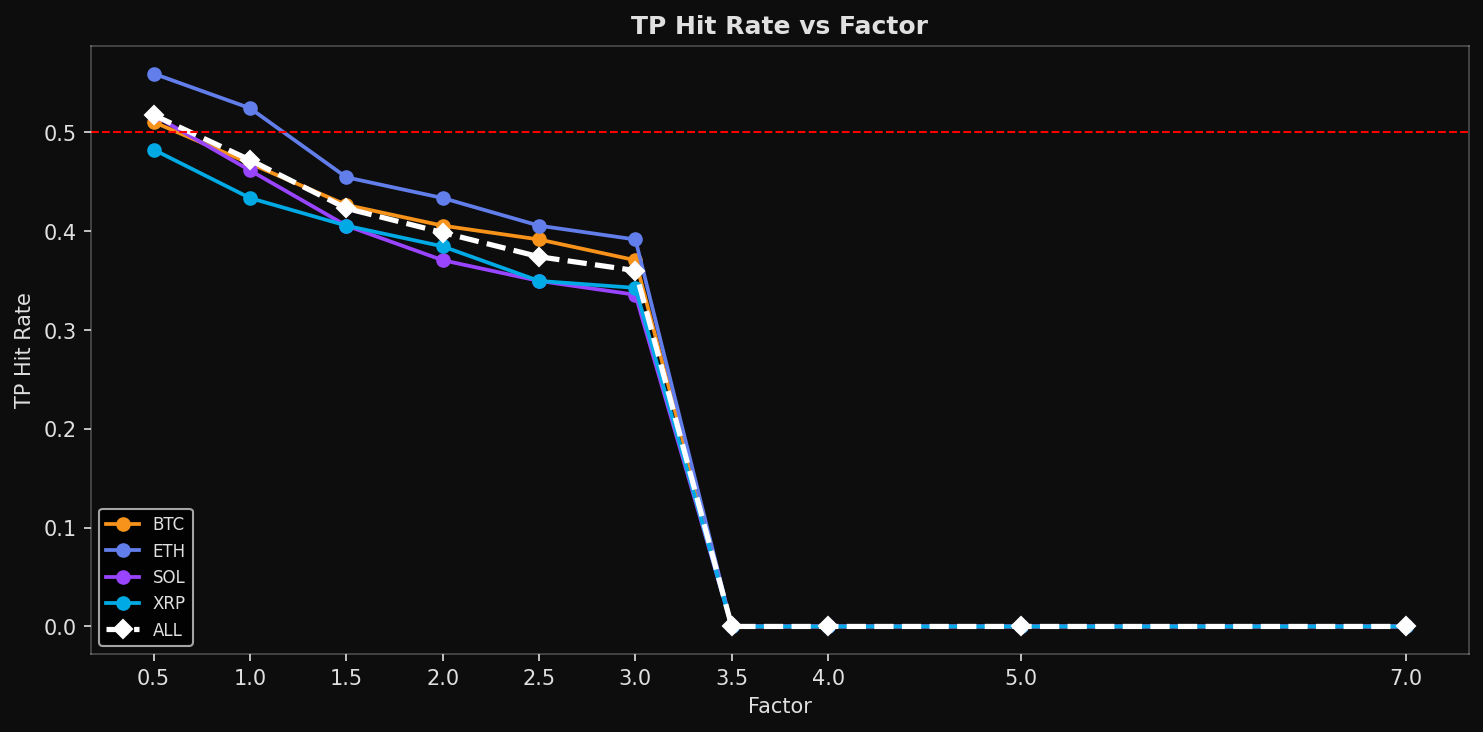

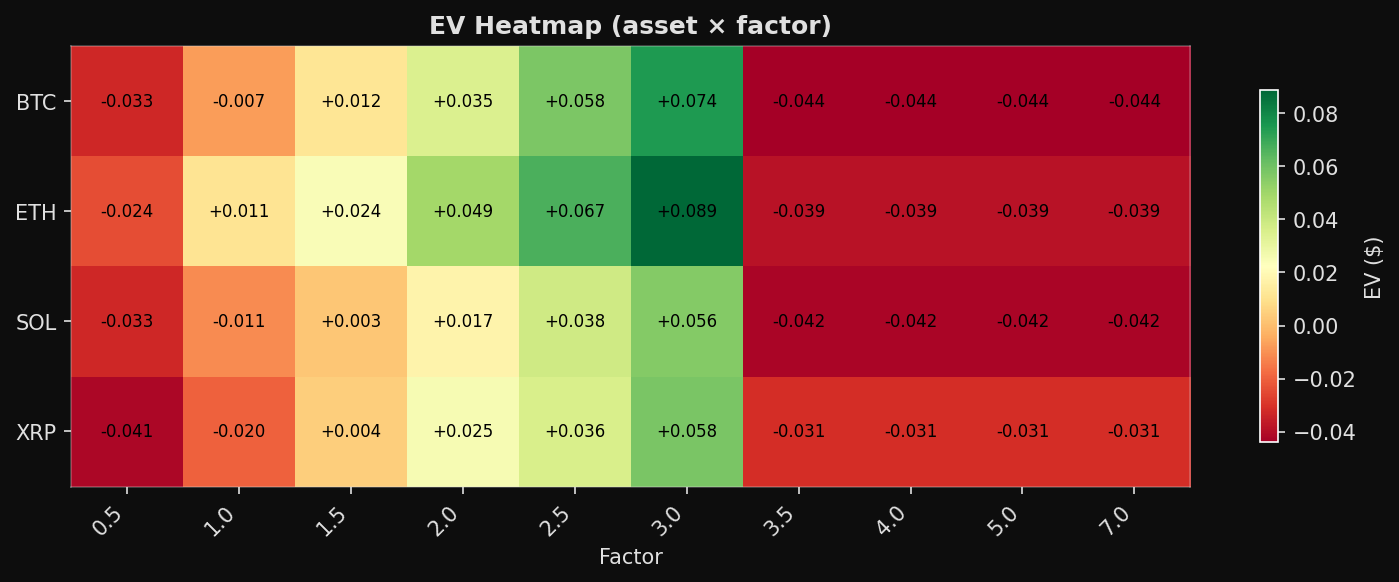

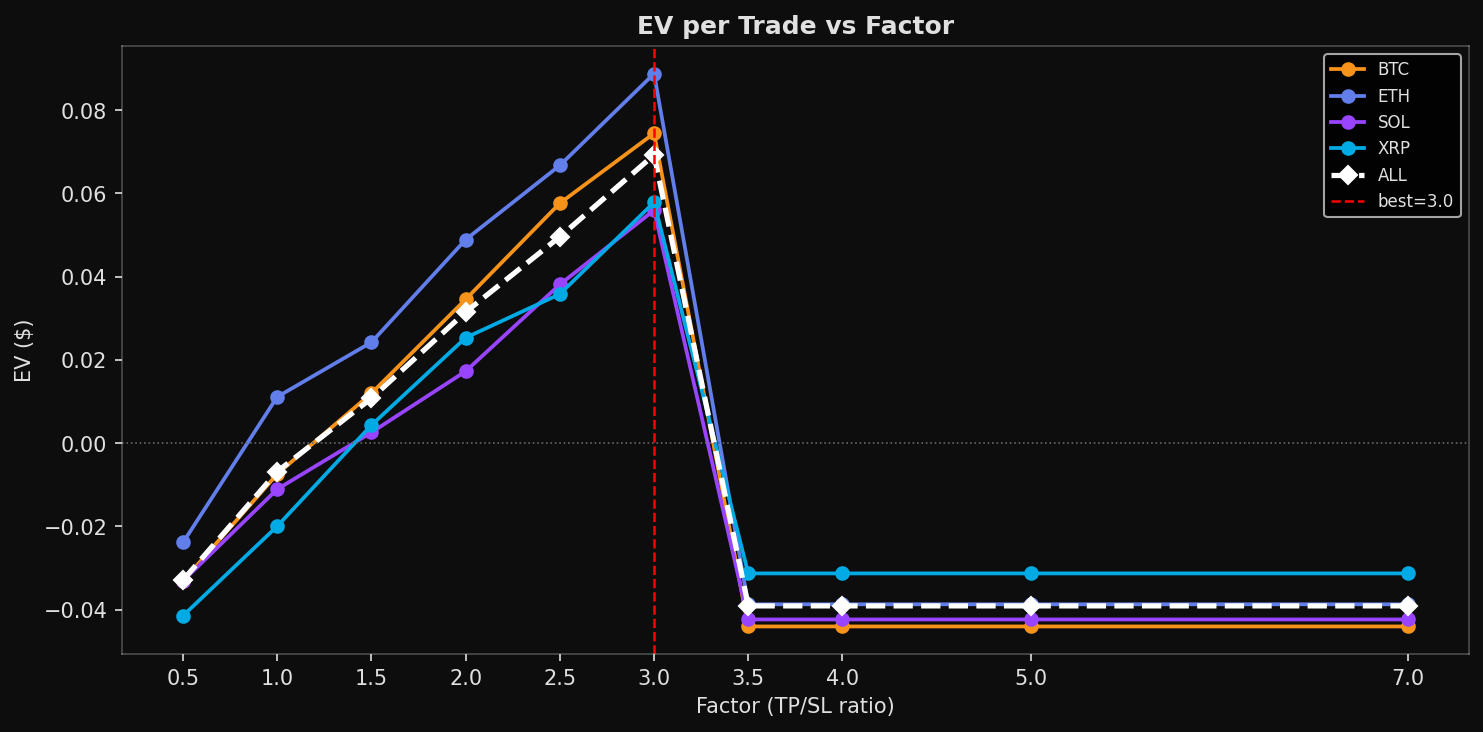

FACTOR SWEEP

The core analysis sweeps the TP:SL ratio (factor) from 0.5 to 7.0 while holding SL fixed at $0.35 and entry at $0.50. Two factor levels are examined in detail:

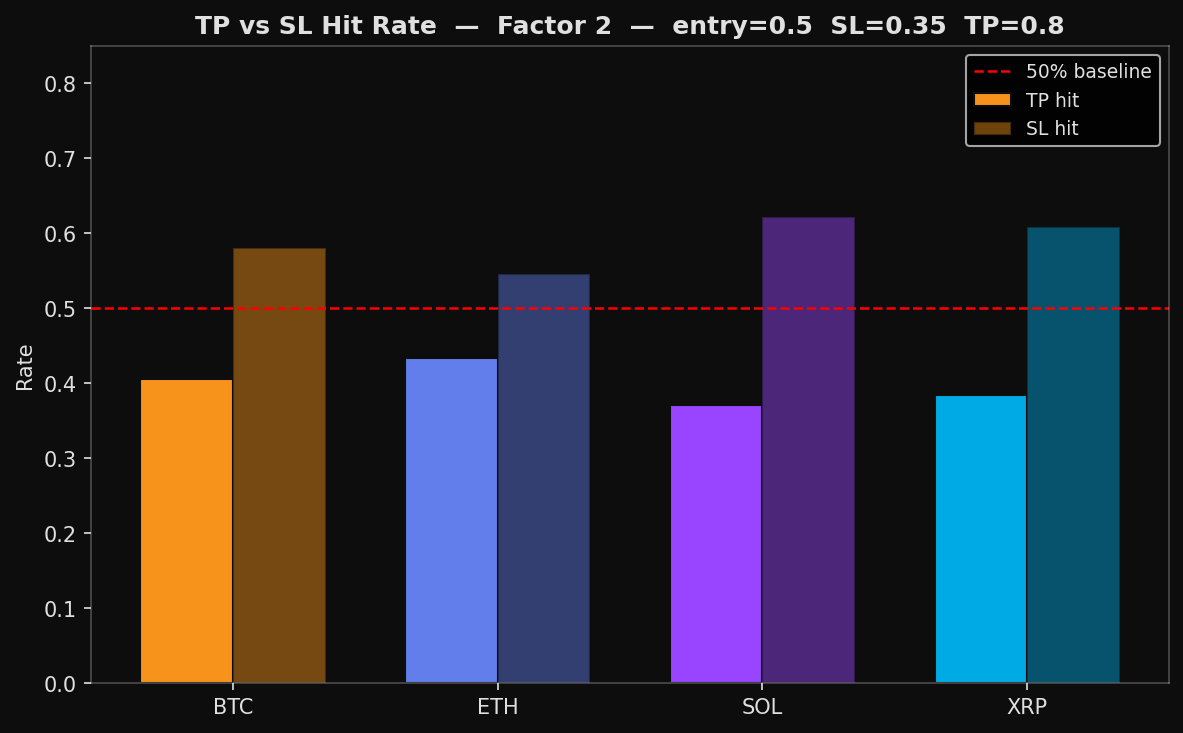

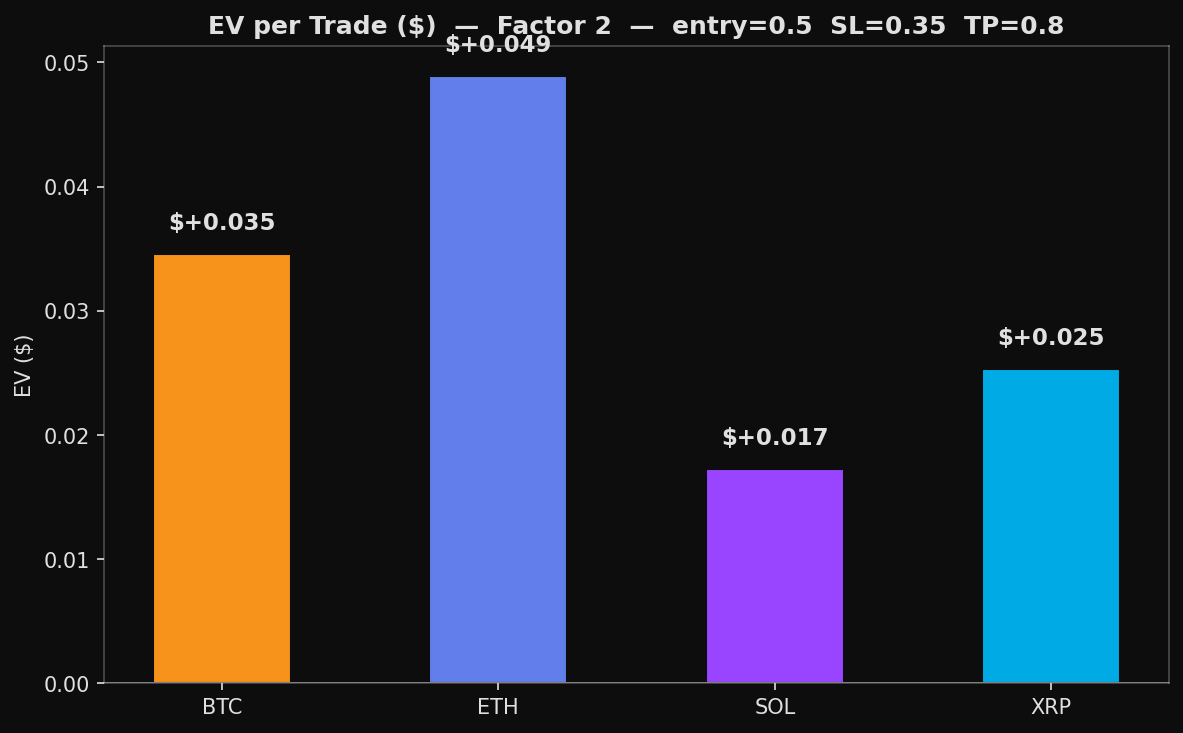

- Factor 2 (TP = $0.80): The stop-loss fires more often than the take-profit across all assets, but the 2:1 payoff asymmetry compensates. All four assets show positive expected value, with ETH leading at +$0.049 per trade.

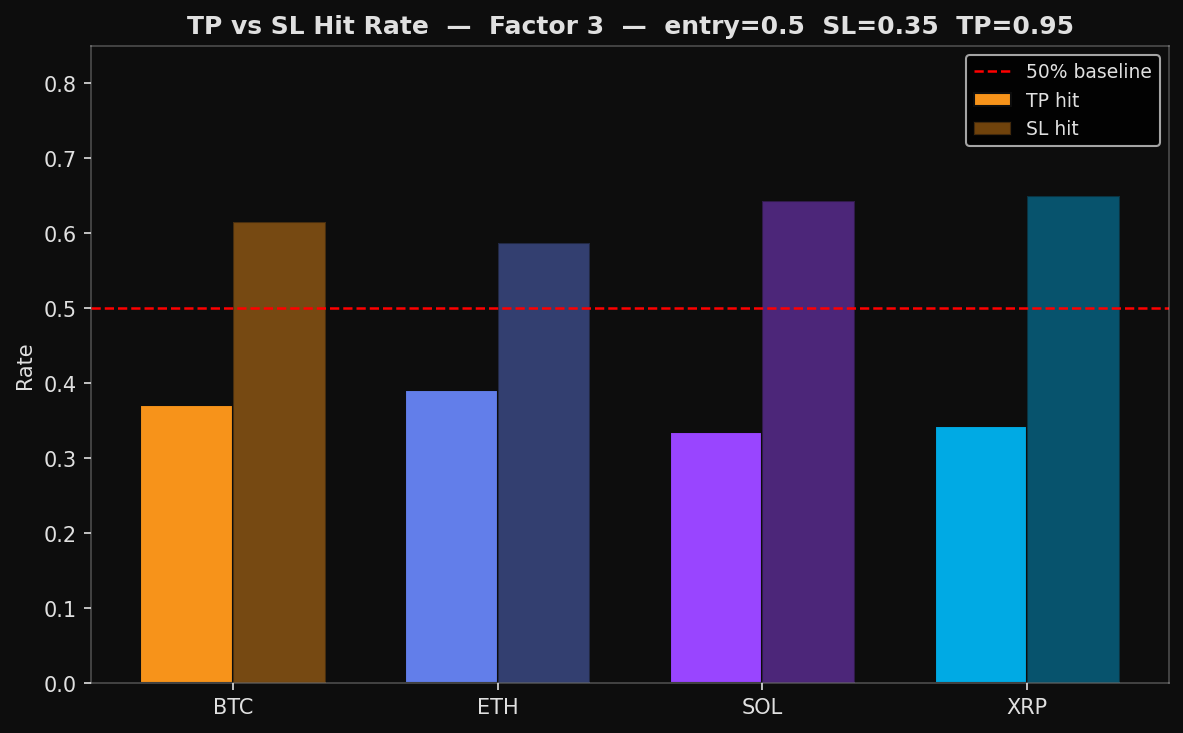

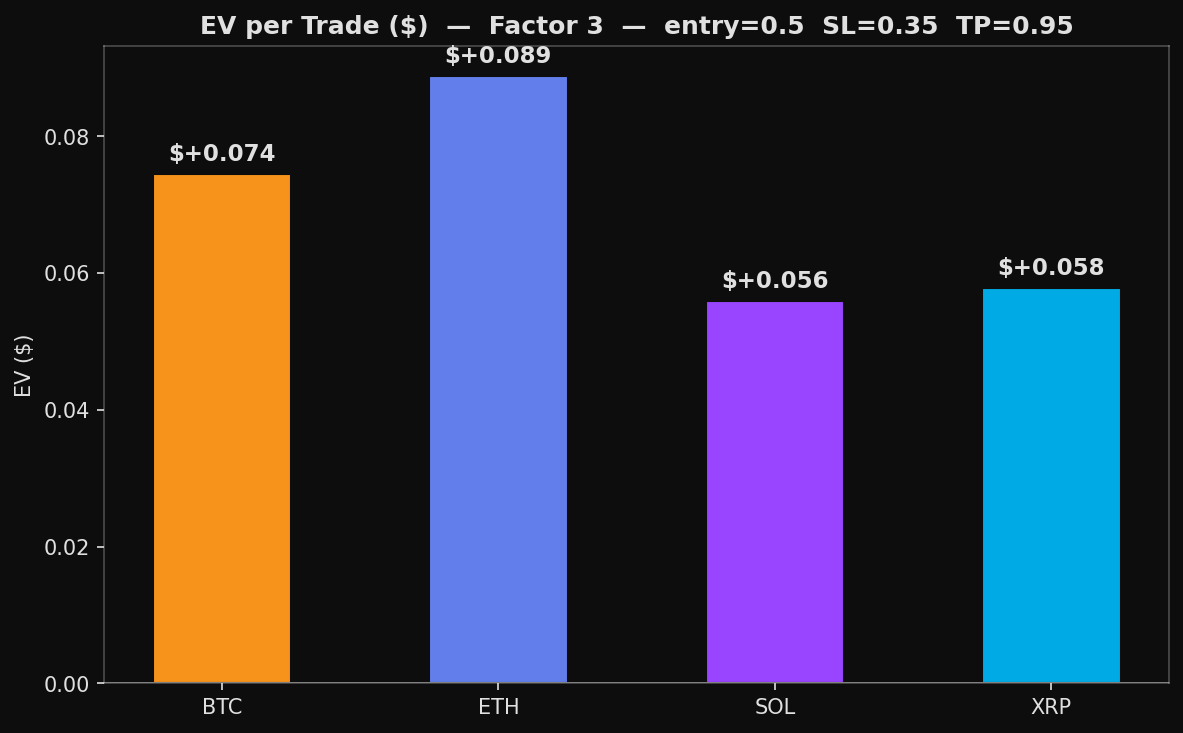

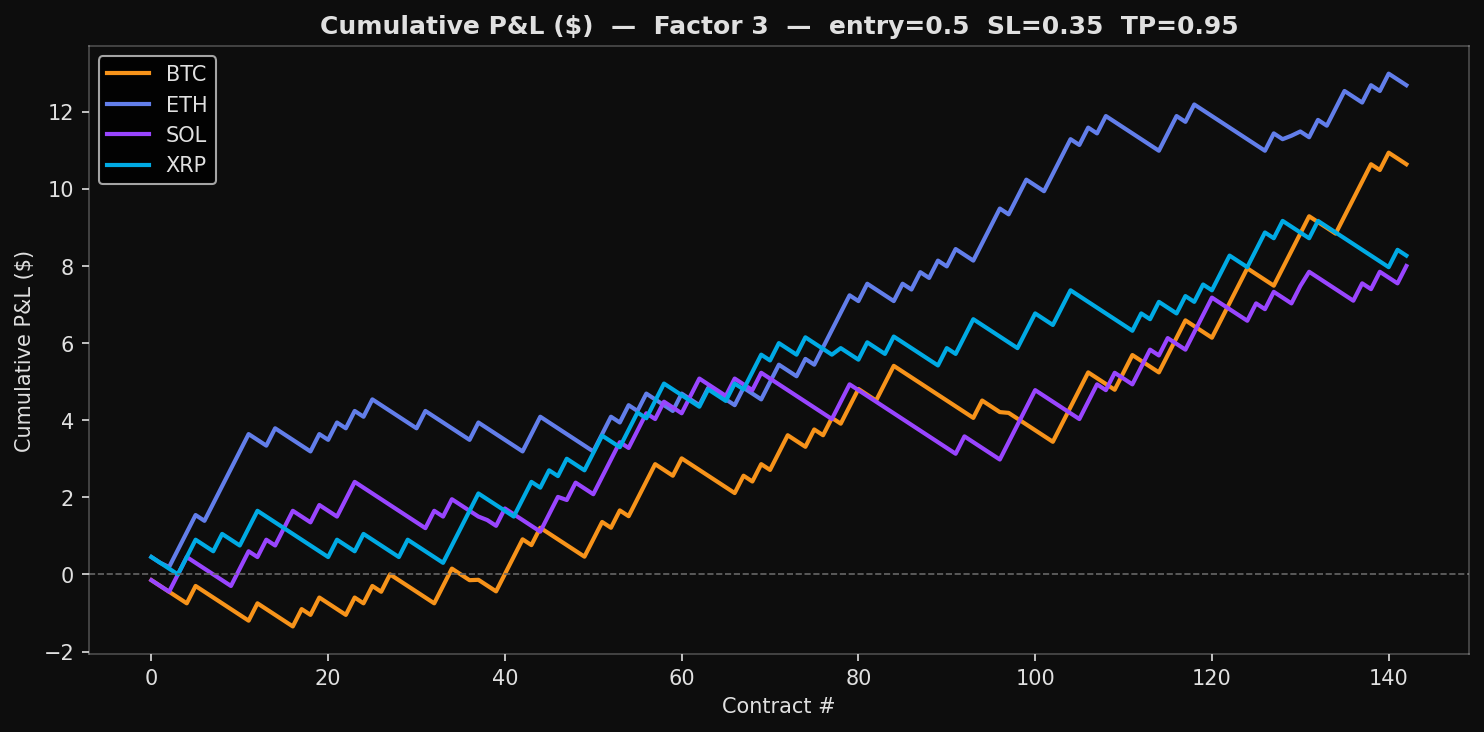

- Factor 3 (TP = $0.95): Higher factor means a wider TP target. The SL fires even more frequently, but each TP hit pays 3x the SL loss. EV increases further, with ETH at +$0.089 per trade.

MONTE CARLO VALIDATION

Ten simulations with different random UP/DOWN assignments across all contracts, using a common bankroll. Each simulation shuffles which side gets picked per contract, confirming that the edge comes from the exit structure rather than side selection. A theoretical Monte Carlo (1,000 simulations of 572 pure coin-flip trades) validates the analytical EV.

KEY TAKEAWAYS

- Positive EV is real: All four assets show positive EV at factors 2–3, consistent across random side assignments.

- Factor 2.5–3.0 is optimal: Beyond factor 3.5, the TP target is too far and rarely triggers, causing EV to collapse.

- The edge is structural: It comes from the asymmetric exit, not from predicting direction. Mirror traders (opposite sides) show similar EV profiles.

- SL on winners is the main cost: A significant fraction of winning contracts dip below $0.35 before recovering, triggering unnecessary stop-losses.

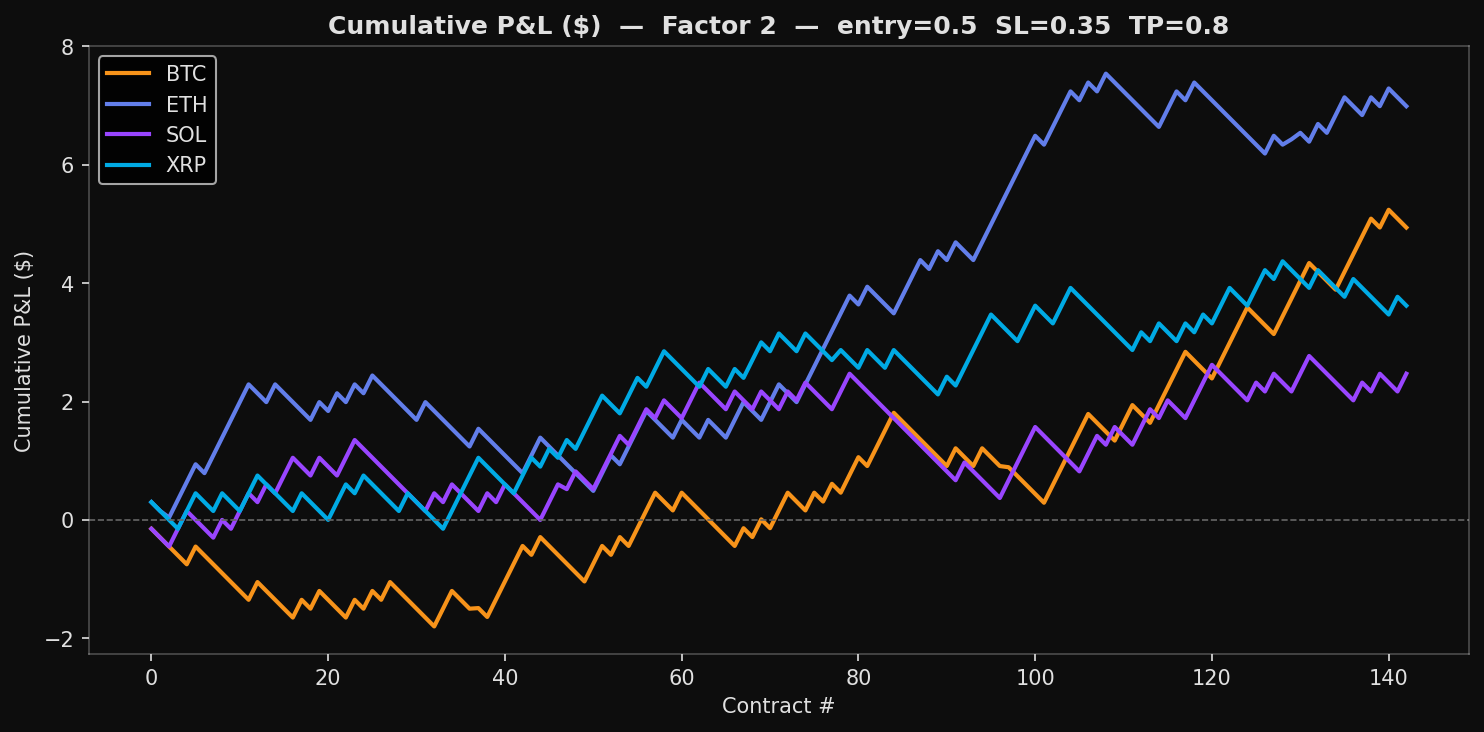

FACTOR 2 ANALYSIS

Entry = $0.50 — SL = $0.35 — TP = $0.80

FACTOR 3 ANALYSIS

Entry = $0.50 — SL = $0.35 — TP = $0.95

HEATMAPS — FACTOR SWEEP

Sweeping TP:SL ratio from 0.5 to 7.0 across all assets